Be Thankful, Grateful, Patient, Charitable, Kind, and don’t forget to smile, as it is infectious. HAPPY VALENTINE’S WEEKEND!!

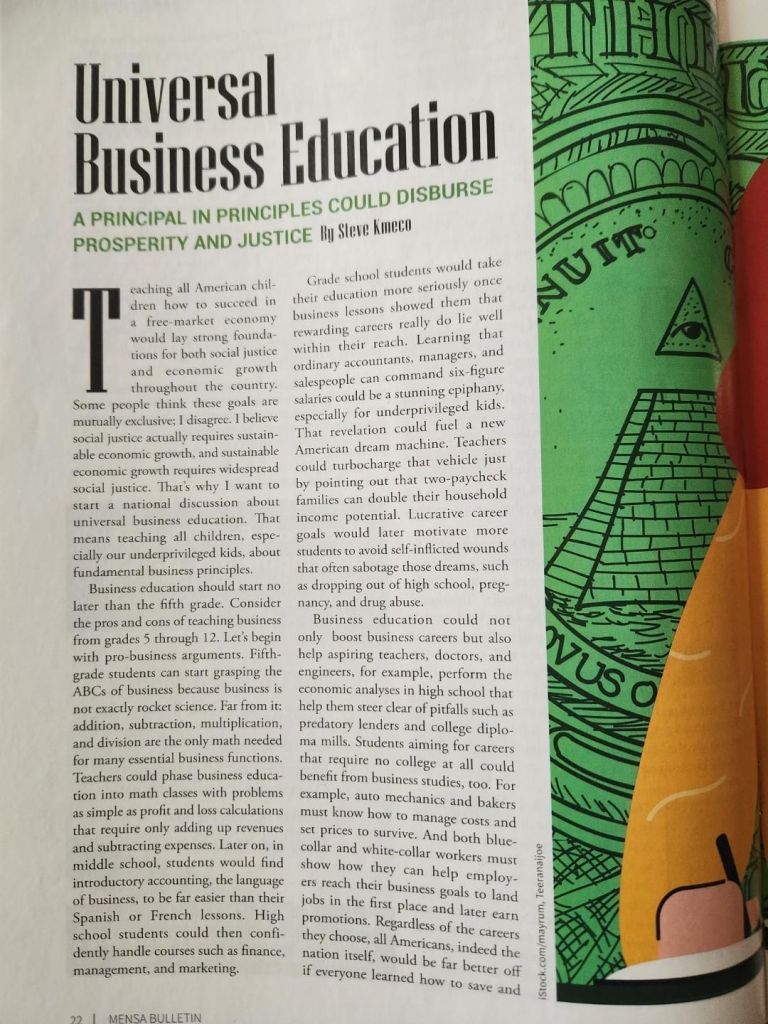

Before I dive into the prompt, I want to pay tribute to my late brother-in-law, Steve Kmeco. He was highly business-savvy and had been a published contributor to MENSA magazine on this topic a few years ago. In his article, Steve outlined the benefits of teaching children as young as fifth grade basic math skills, including addition, subtraction, division, multiplication, and percentages, so they can do just that.

He emphasized the importance of applying these skills to concepts like savings, interest, profit, loss, divestment, compounding, and investment, particularly in relation to 401(k) plans and the stock market. While he acknowledged that not every child would benefit from this teaching approach, he believed that those whose parents are financially savvy could access resources to create wealth from an early age. What kid at that age wouldn’t want to know how to become a millionaire by their thirties?

This situation is similar to parents with children under the age of ten who are taking full advantage of the newly established TRUMP accounts. Our children and grandchildren are mostly older than ten, but it would be something we would’ve taken advantage of. It’s not a political stance; it’s a smart financial strategy, and ultimately, the decision is yours. (Prompt Cont. Below tribute also article published by Steve – Happy Heavenly 71st Birthday Steve)

Try to pay with cash, keeping credit card debt to less than $3,000 on a zero-interest credit card only. Live within your means. Allot funds for Mortgage/rent, gas, food, utilities, car/life insurance, cable, and phone, and don’t forget to pay local taxes on time, as these things affect your credit score. Pay off or reduce the card balance in a short period to maintain a positive credit score. Pay yourself first by putting at least 10% of your net income into an IRA, a Roth IRA, or another managed account with Schwab, Vanguard, or Fidelity. You’ll thank me later if you are not already managing to do so. Also, put another five percent into a savings account as a rainy-day fund, vacation fund, or Christmas fund for unexpected expenses that always pop up in life.

If you are single and living alone, or a single parent, these rules can be a bit harder to manage and may lower expectations in the long term. A suggestion is to take your tax refund and put it into a managed account or a Roth IRA, where you will keep it long-term and compound at a decent rate. Everyone’s life circumstances and income levels differ; the above is only a guideline. Check with a financial adviser or the bank’s services for their input.

Leave a comment